The escort industry operates within one of the most complex payment environments online. Businesses in this sector face increased scrutiny from banks, payment processors, and card networks due to legal ambiguity, reputational sensitivity, higher chargeback risk, and strict compliance obligations.

As a result, accepting payments is far more complicated than simply integrating a payment gateway and enabling transactions for entrepreneurs looking to start an escort business.

Furthermore, escort payment processing depends on a broader financial framework involving acquiring banks, card networks, payment processors, fraud controls, and compliance requirements, all of which directly impact transaction approvals and business stability.

This article explains how escort payment processing works, the systems involved, and the key operational challenges platform owners must navigate to maintain stable and reliable payment operations.

Understanding Payment Processing in Escort Platforms

Every card transaction moves through the same four-party rail .

The merchant (the platform) initiates the charge. The acquiring bank (the merchant’s bank) processes that charge request. The card network (Visa, Mastercard) routes it to the issuing bank (the customer’s bank), which then approves or declines the transaction. Settlement flows back in reverse.

This matters for escort platforms because the risk in this model isn’t distributed equally. The acquirer takes on liability for the merchant’s chargebacks and compliance failures. That’s why high-risk merchant account providers charge significantly higher processing fees. They’re pricing in the probability that they’ll be left holding the bag.

I. MCC and Why They Determine Your Fate

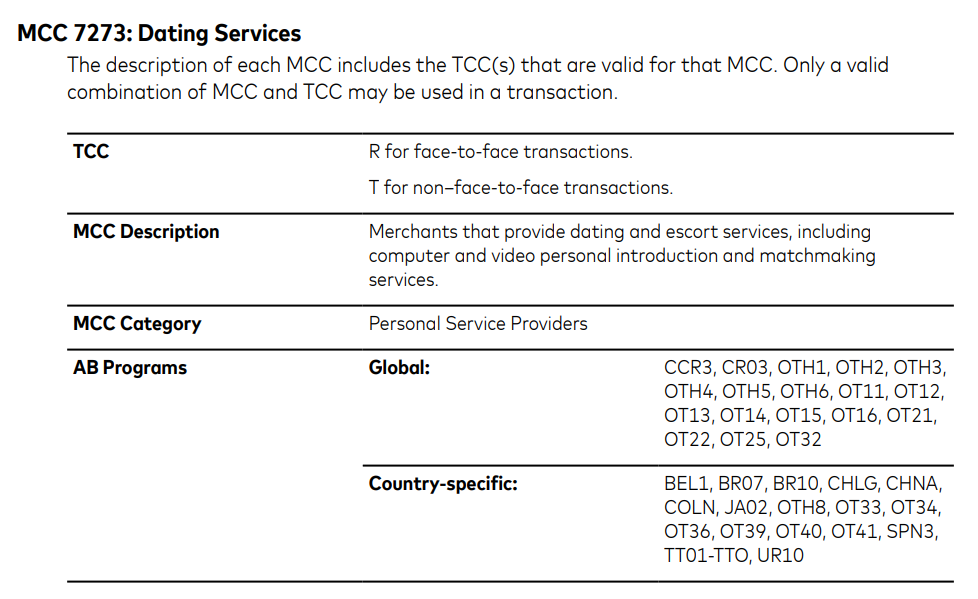

Every business that accepts card payments is assigned a Merchant Category Code (MCC), a four-digit number that tells the card networks what kind of business you are. Escort platforms and adult services typically fall under MCC 7273 (Dating and Escort Services) or adjacent categories.

The structural significance of these codes cannot be overstated, as they form the basis for every risk assessment performed by card networks, processors, and issuing banks. Under Visa’s core rules, specific MCCs are singled out for mandatory high-risk due diligence or total exclusion.

To be classified under MCC 7273 is to operate with an immediate institutional yellow flag; many mainstream processors will trigger an automatic rejection at the policy level before a human underwriter ever opens the file.

II. Payment Gateways vs. Payment Processors vs. Merchant Accounts

Many escort platforms confuse these three terms, and that mistake can lead to critical payment processing issues.

A payment gateway is the technical layer, the API or checkout interface that captures card data and sends it for processing. A payment processor is the company that handles the actual transaction routing between the merchant and the card networks. A merchant account is a special type of bank account that holds funds between the time a transaction is authorized and when it’s settled into your operating account.

For escort platforms, the challenge is that all three of these need to be aligned and willing to work in adult-adjacent categories. Many platforms secure a gateway only to find the processor behind it rejects them at underwriting. Others find processors but can’t get a merchant account from any domestic bank.

III. How Chargebacks Flow Through the System

A chargeback happens when a cardholder disputes a charge with their bank directly, rather than resolving it with the merchant. The issuing bank provisionally refunds the customer, then requests the funds back from the acquirer, who pulls them from the merchant’s account.

For escort platforms, chargeback rates tend to be elevated for reasons we’ll cover in detail later. What’s important here is the structural consequence, processors set chargeback thresholds, typically 1.5% of monthly transactions. Learning how to minimize chargebacks on adult platforms early can significantly reduce the risk of account termination.

If that threshold is breached consistently, the business will be placed into a monitoring program. Breach it further, and your account is terminated and you may be listed on the MATCH file (more on that later part).

IV. The Role of Card Networks and Their Operating Rules

Visa and Mastercard are not banks, they’re network operators. But their rules effectively govern what any bank or processor on their network can do. Both networks publish detailed operating regulations that prohibit certain merchant categories and require enhanced due diligence for others.

Mastercard’s rules around adult content, for example, were significantly tightened after the 2020 New York Times reporting on Pornhub, which led both networks to suspend payments to the platform within days. That event sent a visible signal across the adult industry: card networks will act on reputational risk, and escort platforms sit squarely in the crosshairs.

How Payment Processing Works for Escort Platforms?

The transaction lifecycle for an escort platform booking is more complex than a typical e-commerce checkout. It often involves two separate payment events, the customer payment at booking and the escort payout after service completion.

Between them sits the platform’s exposure window, where a chargeback can hit before funds are fully settled, creating direct financial risk.

Customer Payment Authorization:

The customer enters card details. The payment gateway encrypts the data and sends an authorization request through the processor to the card network, which forwards it to the issuing bank. The issuer checks for available funds, fraud signals, and MCC-based restrictions. Approval or decline comes back in seconds.

Fraud Screening and Risk Scoring:

Most high-risk processors layer their own fraud detection on top of the issuer’s checks. This includes velocity checks (multiple cards from one IP), BIN analysis (prepaid cards flagged differently), device fingerprinting, and 3D Secure authentication. For escort platforms, fraud screening is particularly important because stolen card use is common in anonymous booking contexts.

Settlement Cycles and Fund Holding:

Unlike low-risk merchants who see next-day settlement, high-risk payment processing typically involves 3 – 7 day settlement cycles and rolling reserves, where 5 – 10% of monthly volume is withheld for 90 – 180 days as a buffer against future chargebacks. This is non-negotiable with most acquirers in this space, and founders need to factor it into cash flow projections.

Escrow-Style Systems in Escort Marketplaces:

More advanced platforms use an internal escrow model, where customer funds are held until the booking is completed or the dispute window closes. This reduces chargeback exposure, but it also creates regulatory risk. As holding customer funds may trigger money transmission licensing requirements depending on the jurisdiction. This is why region-specific legal advice is essential before implementing an escrow model.

Subscription vs. One-Time Booking Models:

Recurring billing like selling monthly memberships to escort directories carries a different risk profile than one-time bookings. Subscription chargebacks often spike at the 30-day and 90-day marks when customers forget they signed up. Processors watch subscription chargeback rates separately and may require stricter cancellation flows, email receipts, and clear billing descriptors to reduce disputes.

Payout Flow to Escorts and Platform Commissions:

Paying out escorts or independent providers is a separate compliance problem from accepting payments. Marketplace payout processing for adult platforms requires its own KYC layer for the payee, collecting government ID, address verification, and sometimes tax documentation before funds can be distributed.

Why Are Escort Platforms Classified as High-Risk?

High chargeback probability is the headline reason. Customers dispute charges for a range of reasons unique to this category, embarrassment about the charge appearing on a shared bank account, anonymity-driven regret, misunderstanding of what a “booking fee” covers, or outright fraud using stolen cards. Chargeback rates in adult services consistently run above the 1.5% threshold that card networks use as a trigger point.

Regulatory scrutiny and legal uncertainty add another layer of risk. The passage of FOSTA-SESTA in 2018 changed how platforms connected to adult services are viewed legally. Escort services often sit in a legal grey area in many countries, and that uncertainty makes payment providers far more cautious.

Reputation risk is real and institutional. Banks are publicly accountable businesses with shareholders, regulators, and brand concerns. Even an indirect relationship with escort platforms can create unwanted attention, which many compliance teams prefer to avoid.

Visa and Mastercard compliance requirements also matter. Even if a processor is willing to support an escort platform, it still has to comply with rules set by Visa Inc. and Mastercard Incorporated and those rules can change quickly.

Compared to other high-risk industries like crypto exchanges, online gambling, forex trading, escort platforms face a more severe version of the same structural problem. Crypto and forex, at least, can point to regulatory frameworks (FinCEN registration, CFTC oversight) that signal institutional legitimacy. Escort platforms have no equivalent regulatory badge to present.

Why Most Escort Platforms Get Rejected by Payment Processors?

If your escort platform has been rejected by a payment processor, the reason is rarely random. In most cases, it comes down to a predictable set of risk factors that payment providers actively screen for.

First, many mainstream processors simply prohibit escort-related businesses under their acceptable use policies, regardless of whether the platform operates legally. This broader risk aversion is one of the main reasons payment gateways refuse adult websites and other high-risk businesses altogether.

Beyond policy restrictions, high chargeback rates are a major concern. Escort platforms often experience disputes due to billing confusion, customer regret, or refund abuse, making them riskier to underwrite. Limited proof of service delivery also makes chargebacks harder to defend.

Compliance failures are another common issue. Incomplete KYC documentation, weak age verification, unclear ownership structures, or poor moderation controls can quickly trigger rejection. Finally, fraud risk remains a constant concern.

Platforms handling escort payments must demonstrate strong safeguards such as 3DS2, transaction monitoring, and manual risk reviews to reassure processors that financial and operational risks are being actively managed.

How Payment Providers Evaluate Escort Platforms?

For the minority of processors that do evaluate escort platforms, the underwriting process is more invasive than standard merchant onboarding

Business model screening comes first, is this a direct agency, a listings directory, or a two-sided marketplace? Each has different liability exposure. A listings site that charges for advertising rather than bookings is generally viewed as lower risk.

Founder background checks are standard like criminal history, prior business failures, and previous MATCH list entries will typically disqualify an application immediately. Incorporation structure matters too, domestic LLCs or corporations are viewed more favorably than offshore-only entities.

Transaction volume forecasting needs to be realistic. Understating expected volume to get approved, then scaling rapidly, is a common mistake that triggers automatic reviews and account suspensions.

Chargeback risk modeling involves the underwriter assessing your historical dispute rates or stress-testing your model against industry averages. Mastercard’s MATCH program, the terminated merchant database is checked during this process.

Content moderation and age verification systems are increasingly required. Since 2021, Mastercard has mandated that adult content platforms implement age verification and content moderation before they can process cards. Escort platforms seeking card processing are expected to demonstrate similar controls.

📌Pro Tip: Still mapping your payment strategy? Start with our expert guides on adult payment processors, merchant accounts, & crypto solutions to create a smarter, more reliable payment roadmap.

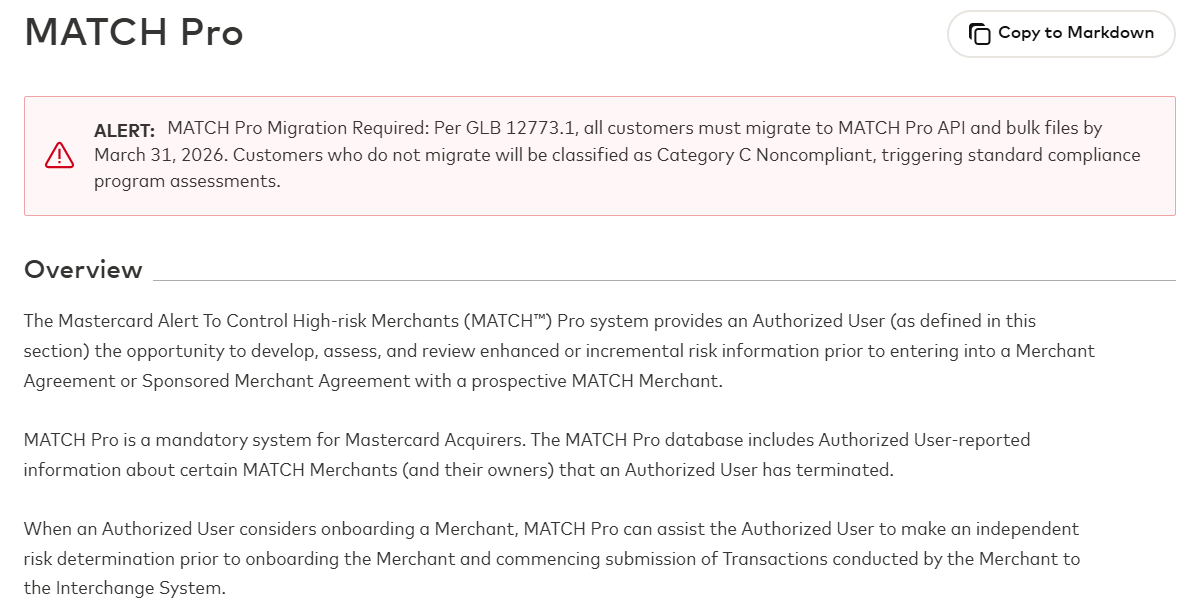

The MATCH File in Escort Industry

The MATCH file which stands for Member Alert to Control High-risk Merchants is a database maintained by Mastercard and used across the card industry. When an acquirer terminates a merchant account for cause, they are required to file the merchant’s details in MATCH within three business days. This database is sometimes called the TMF list (Terminated Merchant File), an older informal name for the same system.

A MATCH listing does not just affect the company. It follows the named beneficial owners and officers personally. A founder who gets listed under one entity and then starts a new company under a different name will still surface in a MATCH check if their personal details match. Every regulated acquirer runs this check during merchant underwriting, and a positive result is almost always a disqualifying finding.

What Triggers a MATCH Listing?

The most common triggers for escort platforms are excessive chargeback activity (crossing Mastercard’s 1.5% threshold), violation of card network operating rules, including misrepresenting your MCC at onboarding and processing transactions that violate applicable laws.

A listing persists for five years and there is no automatic appeals process. Acquirers can correct an entry made in error, but they are under no obligation to do so.

How to Avoid a MATCH Listing?

The most reliable protection is staying well below the 1.5% excessive chargeback threshold and engaging proactively with your processor when dispute volumes begin rising. Acquirers who exit a relationship through mutual termination rather than a for-cause termination are not required to file a MATCH entry.

That distinction between negotiated exit vs. forced termination is one of the most important levers platforms have. It requires maintaining an open relationship with your processor rather than going silent when things go wrong.

Final Thoughts

Building an escort platform is not just a product challenge, it is a payments challenge. The right payment structure, risk controls, and compliance setup can determine whether your platform scales or gets shut down. Founders who understand this early build stronger, more resilient businesses. If you are launching or upgrading an escort marketplace, now is the time to invest in software built specifically for this industry. xScorts by Adent.io is one of the best escort agency software for building a secure, scalable escort platform, offering marketplace-ready features, built-in payment flexibility, and the tools needed to operate confidently in a high-risk environment.

FAQs on Payment Processing for Escort Platforms

1. Do escort platforms need age verification for payment approval?

Yes! Age verification and content moderation are increasingly expected, especially after Mastercard Incorporated tightened its rules around adult content, raising standards across the adult services industry.

2. How does an internal wallet or credit system help escort platforms reduce chargeback risk?

Customers purchase credits first, then spend them on bookings. This creates distance between the card transaction and the actual service, lowering direct chargeback exposure on individual bookings significantly.

3. What cash flow problems do rolling reserves create for growing escort platforms?

With 5 – 10% of monthly volume withheld for up to 180 days, fast-growing platforms can find significant capital locked up at any given time. Founders must factor this into operating budgets before scaling transaction volume aggressively.